A Medicare PFFS plan is a Medicare Advantage (Part C) health plan offered by a private insurance company that contracts with Medicare to provide your Part A and Part B benefits, plus any extra benefits the plan chooses to include. These plans are different from Original Medicare and from Medigap (Medicare Supplement) policies, even though the name sounds similar to “fee‑for‑service.”

Under a PFFS plan, the insurance company—not Medicare—decides how much it will pay for each covered service and how much you pay when you receive care. You must still pay your Part B premium, and most PFFS plans also charge their own monthly premium, although some may be as low as zero additional premium in competitive markets.

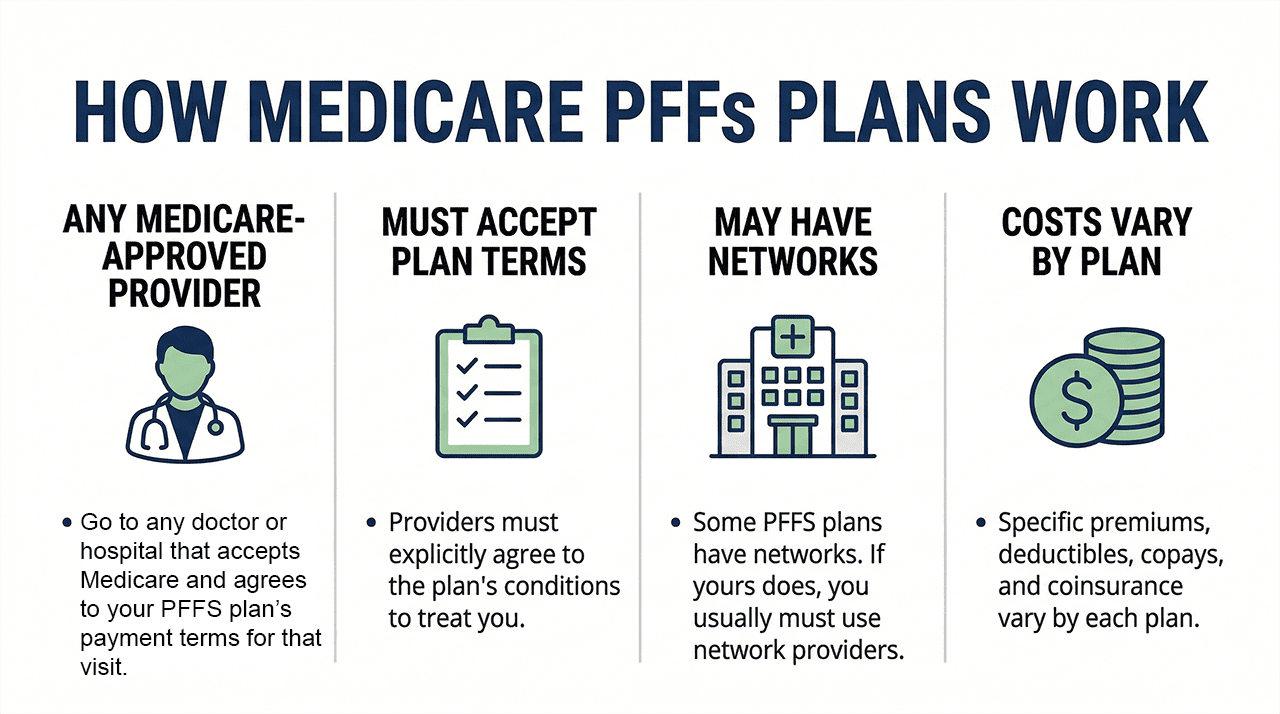

How PFFS Plans Work in 2026

With a PFFS plan, you can see any Medicare‑approved doctor, hospital, or other provider that:

-

Accepts Medicare.

-

Accepts the plan’s payment terms and conditions for that visit.

-

Has not opted out of Medicare for Part A and B services.

Many PFFS plans now operate with a network:

-

Network PFFS plans have a list of providers who have agreed in advance to always accept the plan’s terms and treat members.

-

Non‑network PFFS plans allow you to see any Medicare‑approved provider nationwide who agrees to the plan’s terms each time you receive care, but the provider can decide case‑by‑case whether to accept the plan.

If a provider does not agree to the plan’s terms, the plan generally only has to pay for emergency or urgently needed services from that provider. In a true emergency, any provider must treat you and the PFFS plan must cover emergency care according to its rules.

Provider Acceptance and Balance Billing

One of the most important practical issues with PFFS plans is provider acceptance at the point of service. Each time you visit a doctor or facility, the provider can:

-

Confirm they accept your PFFS plan’s terms for that visit, or

-

Decline to accept the plan’s payment terms and choose not to treat you as a plan member.

Your plan ID card usually includes language telling providers how to verify terms and submit claims, but it is still a good idea for members to ask the provider’s office to confirm acceptance before receiving non‑emergency care.

Many PFFS plans allow “balance billing,” where a provider can charge up to 15% above the amount the plan approves for a covered service, and you are responsible for paying that additional amount. This can increase your out‑of‑pocket costs, especially if you frequently see out‑of‑network or high‑cost specialists.

However, PFFS plans cannot charge more than Original Medicare for certain major services, including:

-

Chemotherapy.

-

Dialysis.

-

Skilled nursing facility care (SNF).

These protections limit cost exposure in some of the highest‑cost care situations.

Networks and Availability Rules

Since 2011, non‑employer PFFS plans offered in “network areas” (counties where at least two network‑based Medicare Advantage plans operate) must maintain a contracted provider network that meets CMS adequacy standards. In those areas, the plan cannot rely solely on the “any willing provider” model; it must show CMS that beneficiaries have reasonable access across major provider categories.

In practice, this means:

-

In urban and suburban counties with many MA plans, PFFS plans typically look and feel more like PPO‑style network plans, with contracted providers and out‑of‑network options.

-

In rural areas with fewer MA choices, PFFS plans may lean more on their ability to pay any Medicare‑approved provider willing to accept the terms.

Availability of PFFS plans varies widely by county and state, and many markets now have few or no PFFS options as HMOs and PPOs dominate Medicare Advantage enrollment. Beneficiaries should use the official Medicare Plan Finder during open enrollment to see if any PFFS plans are available in their ZIP code for 2026.

Costs and Out‑of‑Pocket Limits in 2026

Like other Medicare Advantage plans, PFFS plans in 2026 must include an annual out‑of‑pocket maximum (MOOP) for Part A and B services. For 2026:

-

The maximum in‑network MOOP allowed for MA plans, including PFFS, is $9,250 for Part A and B services.

-

Many plans set lower limits, especially in competitive counties, but this varies by carrier and region.

PFFS plan costs typically include:

-

The monthly Part B premium (standard amount is $202.90 per month for most beneficiaries in 2026).

-

Any additional monthly plan premium the PFFS carrier charges (some may be $0 additional premium).

-

Copays or coinsurance for doctor visits, hospital stays, and other services, set by the plan.

-

Possible balance billing up to 15% above the plan’s allowed amount for some services, if the provider chooses to bill extra.

Because PFFS cost‑sharing is set by the plan and can differ from Original Medicare, members must review the plan’s Evidence of Coverage and Annual Notice of Change each year to see how their costs may change for 2026.

Drug Coverage and Extra Benefits

Some PFFS plans include Part D prescription drug coverage (these are MA‑PD PFFS plans), while others do not. If a PFFS plan does not include drug coverage, you can usually enroll in a standalone Part D plan, unlike with some other MA plan types that may limit this option.

Beyond basic Part A and B services, many PFFS plans offer extra benefits similar to other Medicare Advantage plans, such as:

-

Routine dental, vision, and hearing services.

-

Over‑the‑counter allowances.

-

Fitness memberships.

-

Transportation to medical visits.

-

Supplemental benefits for chronically ill members, where allowed.

Starting with coverage year 2026, CMS is enhancing how supplemental benefits are displayed on the Medicare Plan Finder, showing in‑network and out‑of‑network cost sharing and authorization requirements for a standardized list of benefits. This makes it easier to compare PFFS extra benefits to those of HMOs and PPOs in your area for the 2026 plan year.

2026 Policy and Regulatory Updates Affecting PFFS Plans

PFFS plans are subject to the same broad Medicare Advantage regulations and 2026 policy changes that affect other MA plans. Several updates are important for beneficiaries:

-

The 2026 Medicare Advantage and Part D final rule, issued in April 2025, includes changes around Part D benefit design, the Medicare Prescription Payment Plan, and star ratings that indirectly affect MA‑PD PFFS plans and their formularies and cost structures.

-

CMS continues to refine rules on marketing, prior authorization, and supplemental benefits across MA plans; PFFS plans must comply with these same standards.

-

The Medicare Drug Price Negotiation Program is gradually influencing Part D drug pricing, which may affect premiums and cost‑sharing in PFFS plans that include drug coverage in 2026 and beyond.

Although these rules are not specific only to PFFS, they shape how PFFS plans design benefits, manage utilization, and set premiums for the 2026 contract year.

Advantages of Medicare PFFS Plans

PFFS plans can be attractive for certain beneficiaries because they offer a blend of flexibility and Medicare Advantage extras. Potential advantages include:

-

Provider flexibility: You can see any Medicare‑approved provider that agrees to the plan’s terms, which may help if you travel frequently or live part‑time in different states.

-

No referrals required: You generally do not need a primary care doctor or referrals to see specialists, unlike many HMO plans.

-

Extra benefits: Many PFFS plans include benefits like dental, vision, hearing, and fitness, which Original Medicare does not cover.

-

Out‑of‑pocket cap: Like other MA plans, PFFS plans include an annual out‑of‑pocket maximum, providing a ceiling on Part A and B costs, which Original Medicare lacks.

For the right person, especially someone whose providers are comfortable accepting PFFS terms and who wants more freedom than a typical HMO, these plans can be a workable option.

Disadvantages and Risks to Consider

Despite their potential benefits, PFFS plans come with several key drawbacks and uncertainties:

-

Provider uncertainty: Providers can decide on each visit whether to accept your PFFS plan, so there is less predictability than with a traditional HMO or PPO network.

-

Balance billing: In many PFFS plans, providers can charge up to 15% above the plan’s allowed amount, and you are responsible for the difference, increasing your out‑of‑pocket exposure.

-

Complexity for providers: Some providers are not familiar with PFFS rules or may choose not to deal with them, especially in areas dominated by HMOs and PPOs.

-

Variable availability: In many markets, there are few or no PFFS plans available, limiting choice and making plan continuity over many years less certain.

-

No use of Original Medicare card: When you are enrolled in a PFFS plan, you generally must use your plan card, not your red‑white‑and‑blue Medicare card, and Original Medicare does not pay for your covered care while you’re in the plan.

Because of these factors, PFFS plans are often best suited for informed consumers who are willing to verify provider acceptance and carefully track their costs.

Enrollment, Switching, and Consumer Protections

You can enroll in or switch Medicare PFFS plans during the same periods you can change other Medicare Advantage coverage:

-

Initial Enrollment Period when you first become eligible for Medicare.

-

Annual Enrollment Period (October 15–December 7) for coverage effective January 1.

-

Medicare Advantage Open Enrollment Period (January 1–March 31) if you are already in an MA plan and want to switch or return to Original Medicare.

If you enroll in a PFFS plan that does not include drug coverage, you can generally choose a standalone Part D plan, and you should do so during available enrollment periods to avoid late enrollment penalties.

CMS requires all MA plans, including PFFS plans, to provide written plan documents, standardized summaries of benefits, and access to appeals and grievances processes if you disagree with coverage decisions or encounter problems with the plan. Star Ratings posted on Medicare.gov for the 2026 year give you a way to compare each plan’s quality, customer service, and member experience.

Who Might Consider a PFFS Plan in 2026?

A Medicare PFFS plan may be worth considering if:

-

Your preferred doctors or facilities are familiar with and consistently accept a specific PFFS plan’s terms.

-

You want more flexibility than a typical HMO, but you are comfortable confirming provider participation before non‑emergency visits.

-

You value extra benefits like dental and vision and want an out‑of‑pocket cap, but you either cannot or do not want to buy a Medigap policy.

On the other hand, you might lean toward a different option—such as a local HMO, PPO, or Original Medicare with a Medigap policy—if you prioritize provider stability and dislike the idea that providers can decline your plan or balance bill you.

PFFS Plans Compared to Other Medicare Options

The table below summarizes how PFFS plans compare with other common Medicare choices in 2026.