Treat Medicare like an annual tune-up. Each fall, review your plan’s changes, Part D formulary and tiers, premiums, and provider networks. Compare Medigap F (if eligible), G, and N—benefits are standardized, but rates vary and premiums can rise. Consider switching carriers or plans to save, noting underwriting rules. Use your ANOC letter, list your doctors and drugs, and check prices on Medicare’s Plan Finder between Oct 15–Dec 7. You’ll avoid surprises and uncover smart ways to cut costs next year.

Check These Out

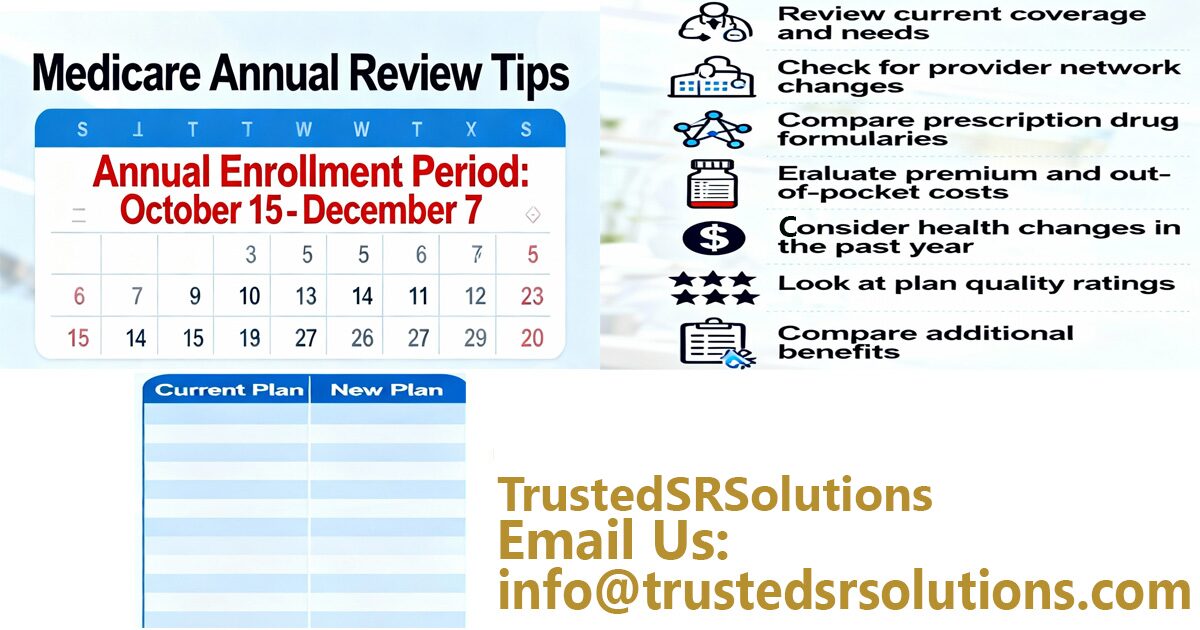

- Open your Annual Notice of Change by October 15 to spot premium, benefit, network, and formulary changes for next year.

- During Oct 15–Dec 7, compare plans’ premiums, deductibles, copays, and maximum out-of-pocket to protect your budget.

- Review Part D drugs: confirm each medication’s formulary status, tier, restrictions, and pricing using Medicare’s Plan Finder.

- Reassess Medigap: benefits are standardized but premiums vary; compare carriers and consider switching plan letters (e.g., F to G, G to N).

- List your doctors, hospitals, and pharmacies to verify they’re in-network or accepted by your chosen plan for the coming year.

Why Annual Medicare Checkups Matter

Even if your coverage felt fine last year, Medicare isn’t set‑and‑forget. Plans, prices, and networks change annually, and missing updates can cost you money or limit care.

Each fall, review your options during the Annual Enrollment Period to confirm doctors, hospitals, and prescriptions still fit.

Check your Part D plan’s formulary and tiers; drugs move, costs shift, and deductibles adjust.

Watch for your Annual Notice of Change letter; it outlines premium, benefit, and network changes. If your plan drops providers or perks, switch.

Don’t assume last year’s choice remains best. A quick yearly checkup protects access and your budget.

Reviewing Supplemental (Medigap) Plans: F, G, and N

While supplemental (Medigap) coverage doesn’t change benefits year to year, you should still review your Plan F, G, or N for price and fit.

Premiums can rise, discounts can change, and your healthcare usage may shift. Confirm your plan type: F (only if Medicare-eligible before 1/1/2020), G (you pay the Part B deductible, currently $257), or N (lower premiums but possible copays and excess-charge exposure).

Check your current premium, household or EFT discounts, and any rate increases.

Compare carriers’ rates for the same plan letter in your ZIP code. Ensure the plan still matches your doctors, travel needs, and budget tolerance for predictable vs. variable costs.

Switching Medigap Plans and Carriers to Save Money

Two proven ways to cut Medigap costs are switching plan letters (e.g., F to G or G to N) and switching carriers for the same plan.

Coverage stays standardized, but premiums don’t—so shop rates. If you’re on Plan F and were Medicare-eligible before 2020, compare Plan G; you’ll trade the now-$257 Part B deductible for often lower premiums.

Prefer fewer copays? Choose G over N; prefer lower premiums and don’t mind office visit copays and possible Part B excess charges? Consider N.

Outside your initial window, most switches need medical underwriting. Compare rates at metagapcompare.com, review underwriting rules, and switch only when savings outweigh trade-offs.

Part D Drug Plans: Formulary and Tier Changes to Watch

You’ve trimmed Medigap costs; now turn to your Part D drug plan, because formularies and tiers can shift every year and hit your wallet.

Review your plan’s Annual Notice of Change. Confirm each medication is still covered and note tier moves—Tier 1 generics cost less; Tier 5 specialty drugs cost most.

Check prior authorizations, step therapy, and quantity limits that could delay fills or increase costs. Compare preferred pharmacies for lower copays and mail-order options.

Use Medicare’s Plan Finder to price your exact drug list. If your drugs jump tiers or drop from the formulary, switch plans during Annual Enrollment.

2025–2026 Prescription Cost Caps and Deductible Updates

Big changes are coming to your Part D costs in 2025 and 2026.

In 2025, your total out-of-pocket spending on covered drugs caps at $2,000. In 2026, that cap nudges to $2,100. After you hit the cap, you’ll pay $0 for covered drugs the rest of the year.

Expect the Part D deductible to rise modestly—from $590 in 2025 to about $615 in 2026—though some plans may set lower deductibles.

Review your medications and plan details now. Confirm each drug’s tier, preferred pharmacy pricing, and any prior authorization rules so you avoid surprises and minimize your 2026 costs.

Medicare Advantage Changes and Reading Your ANOC Letter

Wondering what might change in your Medicare Advantage plan next year? Start with your Annual Notice of Change (ANOC). Plans run on yearly contracts, so premiums, deductibles, copays, and max out-of-pocket can shift.

Networks may drop doctors or hospitals. Extras like dental, vision, hearing, and gym benefits can shrink or disappear.

When your ANOC arrives between mid-September and October 15, read it line by line. Compare 2024 vs. 2025 benefits, costs, drug formularies, and network lists.

Flag provider removals, prior authorization changes, and tier moves for your medications. If your plan’s dropped or worsens, note it now so you can evaluate alternatives promptly.

Key Dates and Steps for the Annual Enrollment Period

Two dates drive your Medicare decisions each fall: October 15 to December 7. Use this window to change Medicare Advantage or Part D plans.

Start by opening your ANOC letter (arrives by October 15) to see 2026 changes. List your doctors, hospitals, and prescriptions. Check formularies and tiers, noting the 2025 $2,000 drug cap.

Compare premiums, deductibles, and max out-of-pocket. Verify networks and perks you actually use.

Decide: stay, switch plans, or move between Advantage and Original Medicare (with Medigap underwriting outside initial rights). Enroll by December 7. Your choices take effect January 1.

Save confirmation and recheck ID cards.

Frequently Asked Questions

How Do I Find Unbiased Help Choosing Between Medicare Options?

Start with SHIP counselors and Medicare.gov’s Plan Finder for unbiased guidance. Compare ANOC letters, formularies, networks, and out-of-pocket caps. Avoid agent-only sources; seek multiple quotes. Document medications and doctors. Call 1-800-MEDICARE, verify plans annually during AEP, and confirm providers.

What Documents Should I Gather Before Comparing Plans?

Right off the bat, gather your Medicare card, current plan ID cards, ANOC letter, medication list with dosages, preferred pharmacies, provider list, recent medical bills, monthly premiums, and budget details. You’ll then compare costs, formularies, and networks confidently.

How Do Medicare Savings Programs Affect My Plan Choices?

They reduce premiums, deductibles, and Part D costs, expanding your choices. You’ll prioritize plans coordinating with MSPs, confirm Extra Help drug savings, and check networks and MOOP. Verify eligibility, income/assets, and state rules before switching during Annual Enrollment.

Can I Keep My Retiree Coverage When Changing Medicare Plans?

Yes, you can sometimes keep retiree coverage, but it depends on your employer’s rules. Don’t bet the farm—call HR. Confirm if it’s secondary to Medicare, compatible with Advantage or Part D, and how premiums, networks, and drug formularies change.

How Do Travel or Moving States Impact My Medicare Coverage?

Moving or traveling can change coverage access. With Original Medicare, you’re generally covered nationwide; Medigap follows. Medicare Advantage and Part D are location-specific; moving triggers a Special Enrollment Period. Check networks, ANOC letters, and formularies, and update plans promptly.