To stretch retirement income, track Social Security’s annual COLA (projected ~2.5% for 2025) and verify your AIME/PIA using SSA’s bend points. Weigh claiming at 62 (reduced) versus waiting past FRA for ~8% yearly credits until 70. Plan for Medicare: enroll at 65 unless covered by credible employer insurance; rising Part B and Part D costs can offset COLA. Coordinate start dates, budget a medical reserve, and consider spousal/survivor needs—you’ll see how to align steps next.

Important Facts

- Track annual Social Security COLA and Medicare premium changes; rising Part B and D costs can offset COLA increases.

- Calculate benefits using your 35 highest earning years; verify AIME and PIA using SSA bend points for accuracy.

- Know your Full Retirement Age; claiming at 62 reduces benefits, while delaying to 70 raises payments about 8% per year.

- Enroll in Medicare at 65 unless you have qualifying employer coverage; delaying Part B wrongly can trigger lifetime penalties.

- Coordinate Social Security claiming with Medicare start dates to optimize income, manage premiums, and protect spousal and survivor benefits.

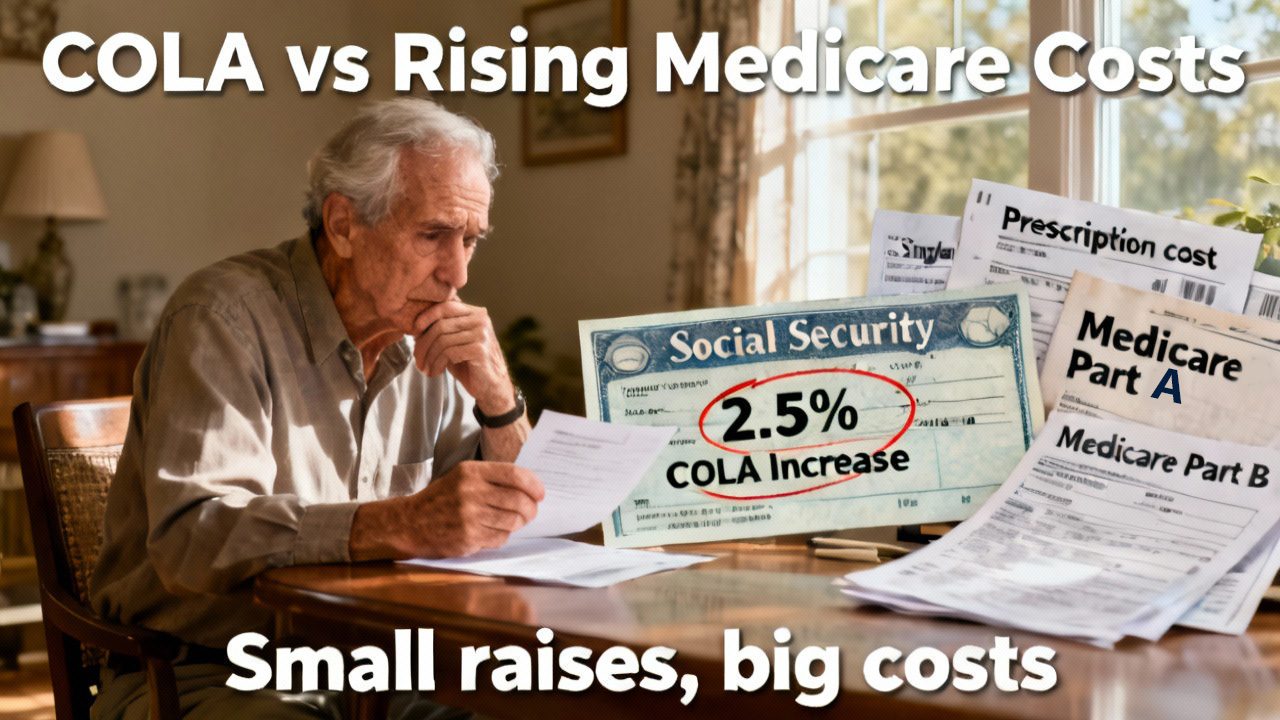

Understanding How COLA Affects Your Benefits

Even though Social Security includes automatic Cost of Living Adjustments (COLA) each year, your monthly increase may feel smaller than expected.

COLA aims to match inflation, but rising prices and Medicare premiums can erode gains. For 2025, a projected 2.5% COLA adds about $57.78 monthly, far below recent spikes like 8.7% in 2023.

Some years, such as 2016, had no increase.

You should plan for gaps. Track finalized COLA announcements and Medicare costs, especially Parts B and D, which can reduce your net benefit.

Build a budget buffer, review insurance options annually, and consider trimming discretionary expenses to protect your monthly cash flow.

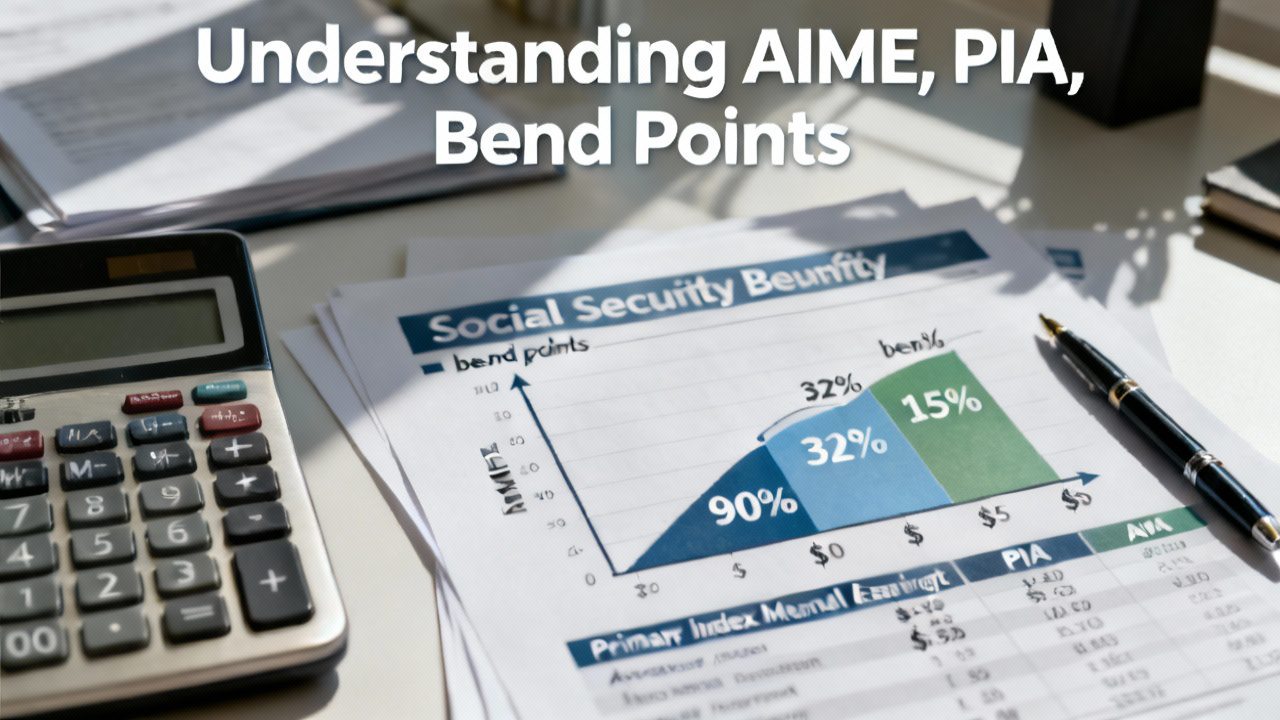

Calculating Your Social Security: AIME, PIA, and Bend Points

While Social Security feels complex, the math behind your benefit is straightforward: it starts with your highest 35 years of earnings, indexed for inflation to create your Average Indexed Monthly Earnings (AIME).

SSA then applies bend points to AIME to compute your Primary Insurance Amount (PIA): 90% of the first $1,226, 32% of AIME between $1,226 and $7,391, and 15% above $7,391.

This progressive formula replaces more of lower earnings and less of higher earnings. Your PIA becomes the base benefit and later gets COLAs.

- Know your indexed earnings history

- Estimate your AIME accurately

- Apply current-year bend points

- Verify SSA’s calculation

Full Retirement Age: Early vs. Delayed Claiming Strategies

Because your filing age permanently shapes your benefit, start by anchoring on your Full Retirement Age (FRA): it’s 66–67 depending on birth year and equals 100% of your PIA.

Claim at 62 and you lock in up to a 30% cut; that reduction lasts for life.

Wait past FRA and you earn delayed credits of about 8% per year until 70, potentially reaching 132% of PIA.

Compare break-even ages: earlier claiming pays sooner, later claiming pays more if you live longer.

Factor spousal benefits, earnings if working before FRA, and survivor needs.

COLA applies regardless, compounding delayed gains.

Projected Medicare Costs and Their Impact on Your Budget

As you plan your retirement cash flow, account for projected Medicare increases that can absorb much of your COLA. A 2.5% COLA—about $57.78 monthly—may be outweighed by higher 2026 costs: Part B’s base could rise toward $265, with deductibles near $285–$288.

Part D’s deductible may reach $615, and the catastrophic cap about $2,100. Build these into your budget now.

- Review your latest Social Security benefit and subtract projected Medicare premiums.

- Compare Part D plans annually; drug tiers and caps shift.

- Set aside a medical contingency fund for surprises.

- Track official updates as final numbers are released.

Social Security Benefits Taxable at Federal or State Levels?

Under existing rules, up to 50% or 85% of your Social Security benefits can be included in your taxable income, depending on your “combined income.” Combined income is defined as:

Adjusted Gross Income (AGI) + nontaxable interest + ½ of your Social Security benefits.

The thresholds are:

If your combined income is below roughly $25,000 (single) or $32,000 (married filing jointly), none of your benefits are taxed.

If your combined income is in between certain ranges, up to 50% of benefits may be taxed.

If your combined income is higher, up to 85% of benefits may be taxed.

Coordinating Social Security With Medicare Decisions

Even small timing choices can change what lands in your bank account each month, so coordinate when you claim Social Security with when you enroll in Medicare.

Your first Medicare window starts at 65; claiming Social Security earlier can trigger Part B premiums sooner and reduce benefits permanently.

Delay claiming, and benefits rise 8% per year until 70, but you’ll still need Medicare at 65 to avoid penalties.

Watch how COLA and Medicare premium changes net out.

If you’re still working, employer coverage might let you delay Part B.

Align start dates to minimize premiums, avoid gaps, and maximize lifetime income.

Where to Get Personalized Guidance and Support

Wondering where to turn for tailored help with Social Security and Medicare? Start with your state’s SHIP (State Health Insurance Assistance Program) for free, unbiased counseling. You can also contact us and we will assist you for free.

Contact Social Security online, by phone, or at a local office for benefit questions, FRA timing, and COLA impacts. Use Medicare’s Plan Finder to compare Part D and Advantage plans, then confirm costs with carriers.

For guided support, schedule a free call with trusted Medicare educators at medicarechool.com.

- Understand how COLA and Medicare premiums affect your budget

- Compare plans and drug costs confidently

- Avoid penalties and enrollment mistakes

- Get ongoing, no-cost expert guidance

Frequently Asked Questions

How Do Remarriage or Divorce Affect Social Security Spousal Benefits?

Remarriage usually ends your divorced-spouse benefits unless you remarry after 60 (50 if disabled). Divorce can qualify you if the marriage lasted 10 years, you’re 62+, unmarried, and your ex’s benefit exceeds yours. Current spouses qualify similarly.

Can I Work While Receiving Benefits Without Reducing Payments?

Yes—if you’ve reached full retirement age, earnings won’t reduce benefits; before FRA, the earnings test may withhold payments. Work more, earn more; paradoxically, benefits pause now, then recalculated higher later, and withheld amounts aren’t lost.

How Do Survivor Benefits Coordinate With My Own Retirement Benefit?

Picture two checks on your table—only one’s cashable. You can’t collect both. You’ll receive the higher of your own benefit or a survivor benefit; if your own grows later, Social Security automatically switches to the larger amount.

What Happens if I Claim and Later Want to Withdraw My Application?

You can withdraw once within 12 months of first claiming. You must repay all benefits paid to you and dependents. Then you can reapply later. After 12 months, you can’t withdraw—only suspend at FRA to earn delays.